What is a Balance Sheet?

The Balance Sheet is a statement that shows the financial position of the business. It records the assets and liabilities of the business at the end of the accounting period after the preparation of trading and profit and loss accounts

‘Not-for-Profit’ Organisations design Balance Sheet for determining the financial position of the establishment. The preparation of the balance sheet is on the same pattern as of the trade entities. It depicts liabilities and assets as during the end of the year. Assets are depicted on the right-hand side, whereas the liabilities are depicted on the left-hand side.

However, there will be a General Fund or Capital Fund in place of the Capital and the surfeit or deficit as per Income and Expenditure A/c which is either deducted from or added to the capital fund, as the scenario may be. It is a common practice to add some of the subsidised items like entrance fees, legacies and life membership fees precisely in the capital fund.

Table of Content

- Features of Balance Sheet

- Importance of Balance Sheet

- Purpose of the Balance Sheet

- How to prepare a Balance Sheet?

- Balance Sheet Format

- Reserve in Balance Sheet

- Consolidation of Balance Sheet

- How to Prepare Consolidated Balance Sheet?

Features of Balance Sheet:

The features of a balance sheet are as follows:

- It is regarded as the last step in final accounts creation

- It is a statement and not an account

- It consists of transactions recorded under two sides namely, assets and liabilities. Assets are placed in the left hand side, while the liabilities are placed on the right hand side

- The total of both side should always be equal

- The balance sheet discloses financial position of the business

- It is prepared after trading and profit and loss account is prepared.

Importance of Balance Sheet:

Balance sheet analysis can say many things about a company’s achievement. Few essential factors of the balance sheet are listed below:

- Creditors, investors, and other stakeholders use this financial tool to know the financial status of a business.

- It is used to analyse a company’s growth by comparing different years.

- While applying for a business loan, a company has to submit a balance sheet to the bank.

- Stakeholders can find out the business accomplishment and liquidity position of a company.

- Company’s balance sheet analysis can detect business expansion and future expenses.

What is the purpose of balance sheet?

The main purpose of the balance sheet is to show a company’s financial status. This sheet shows a company’s assets and liabilities, along with the money invested in the business. This statement is required to analyze the financial status information for several consecutive periods.

Generally, investors and creditors look at the balance sheet of the company to understand how effectively a company will use its resources and how much it can give in return. Though the balance sheet can be prepared at any time, it is mostly prepared at the end of the accounting period. The balance sheet can be created at any time. However, it is often prepared at the end of the financial year.How to prepare a Balance Sheet?

Below are the steps mentioned to prepare a balance sheet.

- Compose a trial balance- It is a regular report included in any accounting programme. If it is a manual mode, then create a trial balance by transferring every general ledger account’s ending balance to a spreadsheet.

- Arrange the trial balance- It is important to arrange the initial trial balance to assure that the balance sheet similar to the relevant accounting structure. While using adjusting entries to adjust the trial balance all the entry should be completely recorded so the auditors can understand why it was made.

- Discard all expense and revenue accounts- The trial balance includes expenses, revenue, losses, gains, liabilities, equity, and assets. Delete all from the trial balance except equity, liabilities, and assets. However, the deleted accounts are used to create an income statement.

- Calculate the remaining accounts- In this stage, sum up all the trial balance account used to create a balance sheet. The typical line items used in the balance sheet are:

- Cash

- Accounts receivable

- Inventory

- Fixed assets

- Other assets

- Accounts payable

- Accrued liabilities

- Debt

- Other liabilities

- Common stock

- Retained earnings

- Validate the balance sheet- The total for all assets recorded in the balance sheet should be similar to the liabilities and stockholders’ equity accounts.

- Present in the required balance sheet format.

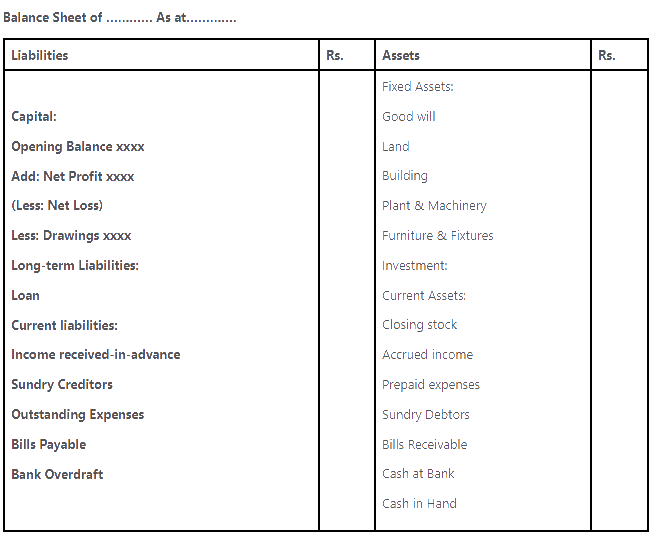

Balance Sheet Format:

The balance sheet of a company will look like the image given below.

What is Reserve in Balance Sheet:

A reserve is a retained earnings secured by a company to strengthen a company’s financial position, clear debt & credits, buy fixed assets, company expansion, legal requirements, investment and other plans. These are usually done to save the cash from being used in other purposes. Reserve funds do not have any legal restrictions so that the company can use it for any purpose. For instance: Let’s consider company ABC has to suspend one of its products and release refunds to its buyers over the periods of six months.

To make sure that the company has enough money to give refunds, a balance sheet reserve of ₹1,00,000 is created. As customers demand refunds, Company ABC reduces the ₹1,00,000 reserve. Especially insurance companies regularly create balance sheet reserves to make sure they have sufficient funds to pay out claims. The reserves usually meet the expense of applications that have been registered but not yet paid. Balance sheet reserves are registered as liabilities on the balance sheet.

Consolidation of Balance Sheet:

A consolidated balance sheet shows both the liabilities and assets of a parent company along with its subsidiaries in one document, without any specific mention about which item is associated with which company. A consolidated financial statement is issued by a company whenever it acquires 50 per cent of controlling stake or business in another company. For example: If an organization has ₹1 million as assets and buy subsidiaries for ₹400,000 and ₹300,000, assets respectively. In this scenario, the consolidated balance sheet will reflect ₹1.7 million as an asset.

While recording the consolidated balance sheet, it’s essential to modify the subsidiaries assets figures so that they indicate the accurate market value. Also, the parent company revenue should not be included in this sheet because the net change is ₹0.

How to Prepare Consolidated Balance Sheet?

To prepare a consolidated balance sheet first name the document, it’s subsidiary and date at the head of the sheet. In the left-side column, create a section for assets, liabilities, and equity. All the numbers included in the sheet should match with the worksheet’s consolidated trial balances. After including the numbers from your worksheet, review the consolidated balance sheet.

0 Comments